Rapid Response - Australian headline CPI cools, core concerns linger

- Brett Careedy

- 13 minutes ago

- 3 min read

Headline CPI inflation eased further in May, helped by falling fuel prices. Underlying inflation told a stickier story, surprising to the upside and hitting the highest annual rate since 2024.

Australian headline CPI inflation eased to +4.0% yoy in the 12 months to May 2026, down from +4.2% in April and below the consensus forecast of +4.3%, according to the ABS.

On a monthly basis, the CPI fell -0.7% in original terms and -0.1% in seasonally adjusted terms.

The trimmed mean measure of underlying inflation rose to +3.6% yoy in May, up from +3.4% in April and above the consensus forecast of +3.5%. Monthly trimmed mean inflation was +0.4%, also above the +0.3% expected. This is the highest annual core inflation rate since Q3 2024.

Housing remained the largest contributor to annual inflation at +6.5% yoy, unchanged from April. Within housing, electricity costs surged +21.1% yoy as Commonwealth and State government rebates continued to wind down.

Transport inflation eased sharply to +3.3% yoy from +6.6% in April. Automotive fuel prices fell -11.9% in May, following a -7.0% decline in April. Rachael McCririck, ABS head of prices statistics, said: "These monthly falls include the impacts of the halving of the fuel excise on 1 April and lower world oil prices in recent weeks."

Food and non-alcoholic beverages rose +3.3% yoy in May, up from +2.8% in April, suggesting some pass-through of earlier energy and logistics cost pressures into the food supply chain.

Annual goods inflation decelerated to +4.2% yoy from +4.7% in April, driven by the moderation in fuel. Annual services inflation rose to +3.7% yoy from +3.5%, the highest in three months.

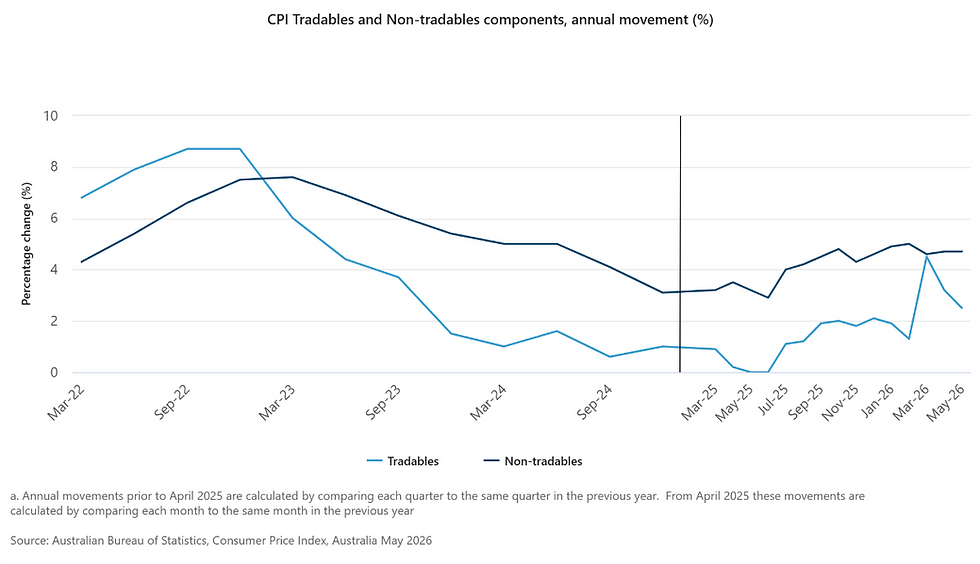

Tradables inflation eased to +2.5% yoy from +3.2%.

Non-tradables inflation remained elevated at +4.7% yoy, unchanged from April, reflecting persistent domestic price pressures. The main contributors were electricity (+21.1%), New dwellings (+5.6%) and Medical and Hospital Services (+5.0%).

S&P/ASX200 8,879 +0.1%, AUDUSD 0.6908 -0.1%, Aus 2yr 4.44% (unch), Aus 10yr 4.76% -1bp

Fin-X Capital View

The headline drop to +4.0% yoy was almost entirely mechanical as the unwinding of the fuel excise cut in April, compounded by lower global oil prices, drove the headline lower.

Underlying inflation moved in the opposite direction, beating expectations. Markets and the RBA should (and likely will) look through the headline and concentrate on core inflation.

Services inflation rising to +3.7% yoy is the most concerning element of today's report. The initial fuel shock, while partly temporary, is beginning to feed through to broader costs, particularly in categories where businesses face higher logistics and input costs. 8/11 groups experienced an annual increase above the RBA's 2%-3% target range.

In its May Statement on Monetary Policy, the RBA projected headline CPI to peak at +4.8% in Q2 2026 and trimmed mean to reach +3.8% by June. Today's data means the headline is tracking materially below that forecast, but the trimmed mean at +3.6% is still on a path that could reach the RBA's Q2 estimate if June comes in firm.

The RBA paused at its June meeting following three consecutive hikes totalling 75bps, and Governor Bullock has indicated the Board wants to assess the impact of that tightening before acting again. A hold in August appears the base case, but with core inflation running above target and services proving sticky, November can't yet be ruled out.

Even if tomorrow's May unemployment figure holds at 4.5% instead of ticking down to 4.4% as expected, a cut seems very unlikely this year, given the +4.75% increase in the minimum wage starting next month.

Disclaimer

The contents of this communication is prepared by Fin-X Capital Group Pty Ltd (A.C.N. 627 650 293; AFSL 520526). The information contained in this communication is general in nature and does not take into consideration any investors personal objectives, goals, needs and financial situation. You should not rely on the information contained in this document to make any investment decisions without first consulting an investment professional such as your financial adviser. Any unauthorised use of this document is prohibited. This document (including any attachments) is intended only for the addressee, it may contain information of a privileged and confidential nature. If you are not the addressee of this communication, you must not copy, reproduce, disseminate or use this email and its contents. If this communication has been received in error by you, please inform us immediately and securely delete. Sharing, transmitting, copying, disseminating all or part of the contents of this document may result in a breach of the Federal Privacy Legislation and or copyright and trademark infringement of Brerona Capital Asset Management Pty Ltd and its related entities.