Fin-X Rapid Response 18th June 2026

- Brett Careedy

- 22 hours ago

- 4 min read

The Federal Reserve did not make any changes to monetary policy today. But the materials revealed that the FOMC was broadly becoming more hawkish. An ambitious reform program was also unveiled.

The Federal Reserve held monetary policy settings steady this morning and issued a much shorter statement: The Federal Open Market Committee approved the following statement for release by a 12 – 0 vote:

The Committee decided to maintain the target range for the federal funds rate at 3-1/2 to 3-3/4 percent, in support of the Federal Reserve's dual mandate. The Committee reaffirmed its policy of maintaining ample reserves in the banking system.

Economic activity is expanding at a solid pace despite elevated uncertainty that owes, in part, to the conflict in the Middle East. Productivity growth and capital investment are strong. Job gains have kept pace with the workforce, and the unemployment rate has changed little.

Inflation remains elevated relative to the Committee's 2 percent goal, in part reflecting supply shocks that have driven price increases in certain sectors, including energy. The Committee will deliver price stability. [Emphasis added]

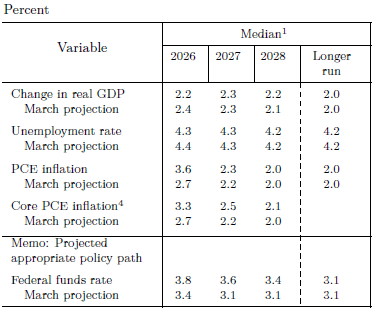

The 2026 real GDP projection was revised -0.2% lower compared to March to 2.2%, while PCE inflation was revised +0.9% higher to 3.6%, but only +0.1% higher in 2027 and still +0.3% above the 2% target.

Core PCE inflation is projected to remain above target over the forecast period from 2026 to 2028.

Unemployment is expected to be slightly lower in 2026, remaining at 4.3% over the next two years and falling to 4.2% in 2028.

The Federal Funds rate is expected to remain at its current level in 2026, where cuts were previously expected. Moreover, although 5 cuts are forecast for next year, the rate is expected to be half a percentage point higher next year than in the March forecasts and a quarter point higher in 2028.

In his official remarks, Kevin Warsh reiterated the economic assessment in the shorter statement and reiterated that, after five years of above-target inflation, "This Committee will deliver price stability." Although he recalled the Fed's dual mandate, the emphasis is clearly on short-term inflation.

He also signalled his intention to work with colleagues to reform the Fed's practices, beginning with a shorter factual statement and removing forward guidance. Although he encouraged his colleagues to complete the Summary of Economic Projections, there was one fewer dot this month as he did not enter projections.

He later added that he wanted financial market prices to provide information on the private sector assessment of the outlook, rather than merely reflecting the Fed's own statements.

The 18 dots entered showed that the projected figures echoed the numerical projections, with more FOMC members leaning towards a rate rise this year. Six members now expect at least one rate rise, although the median projection maintains the rate at 3.75%. The median projection in March was for one quarter-point cut.

In addition, he announced the creation of task forces to work in 5 areas:

Communication

Balance sheet policy

Use and reliance on existing data sources

Productivity and jobs in an era of transformation

Inflation frameworks

He added that he expects them to report by year-end, and that the 2% target is not yet under review.

S&P500 7,420 -1.2%, Nasdaq Comp. 26,022 -1.3%, S&P/ASX200 future 8,892 -0.7%,

US 2yr 4.18% +13bps, US 10yr 4.49 +5bps

US dollar (DXY) index 100.09 +0.6%, AUDUSD 0.7014 -0.8%, Gold US$/oz 4,257 -1.7%

Fin-X View

The headline for today's market is that the committee is leaning more hawkish despite apparent progress on opening the Strait of Hormuz. There was no sign that the new Chair was advocating for cuts in line with President Trump's clear preference, as Stephen Miran had previously done.

Despite some humility in his language, there was nothing humble about Kevin Warsh's planned reforms. The task force programs are ambitious and potentially highly consequential.

In previous comments, Chair Warsh has said that the Federal Reserve has moved beyond the bounds of its mandate. At the press conference today, he mentioned, on more than one occasion, going back to first principles.

The decision to step back from forward guidance is already controversial. Whereas Chair Walsh suggested that financial market pricing should not reflect Fed guidance, the purpose of forward guidance has historically been to influence rates further out along the curve. That might not always be appropriate. But in a future period of stress, it will be interesting to see if that important tool remains in the trash can. Of course, one of the criticisms levelled at the Fed is that forward guidance was overused during the pandemic and not necessarily accurate.

It will take some time for the new direction to become clear, and it is reasonable to expect some discomfort with the scope of the outlined reforms. It remains to be seen whether this will result in higher risk premia being priced into interest rate markets.

Disclaimer

The contents of this communication is prepared by Fin-X Capital Group Pty Ltd (A.C.N. 627 650 293; AFSL 520526). The information contained in this communication is general in nature and does not take into consideration any investors personal objectives, goals, needs and financial situation. You should not rely on the information contained in this document to make any investment decisions without first consulting an investment professional such as your financial adviser. Any unauthorised use of this document is prohibited. This document (including any attachments) is intended only for the addressee, it may contain information of a privileged and confidential nature. If you are not the addressee of this communication, you must not copy, reproduce, disseminate or use this email and its contents. If this communication has been received in error by you, please inform us immediately and securely delete. Sharing, transmitting, copying, disseminating all or part of the contents of this document may result in a breach of the Federal Privacy Legislation and or copyright and trademark infringement of Fin-X Capital Group Pty Ltd and its related entities.