Rapid Response - April Australian CPI inflation better than feared

- Brett Careedy

- 3 days ago

- 3 min read

Slightly better-than-expected CPI figures and slightly worse employment data are likely to keep the RBA on hold for now.

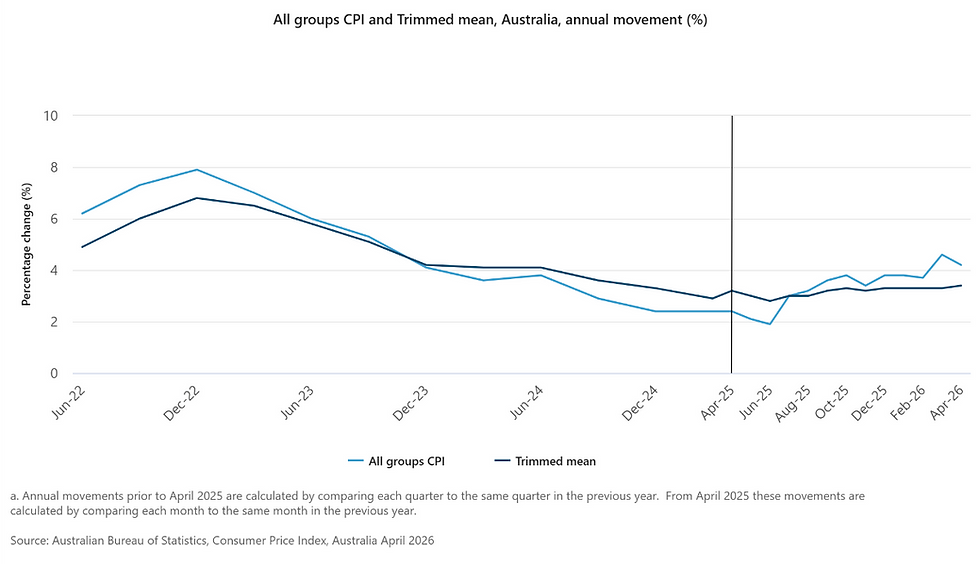

Australian headline CPI inflation receded from +4.6% yoy in March to +4.2% in April. The consensus forecast was for a +4.4% rise in prices.

Monthly inflation also undershot expectations, dropping from +1.1% to +0.4%.

Trimmed mean inflation increased slightly from +3.3% yoy in March to +3.4% yoy, in line with forecasts.

Monthly trimmed mean inflation was in line at +0.3%, with the March number being revised down from +0.3% to +0.2%.

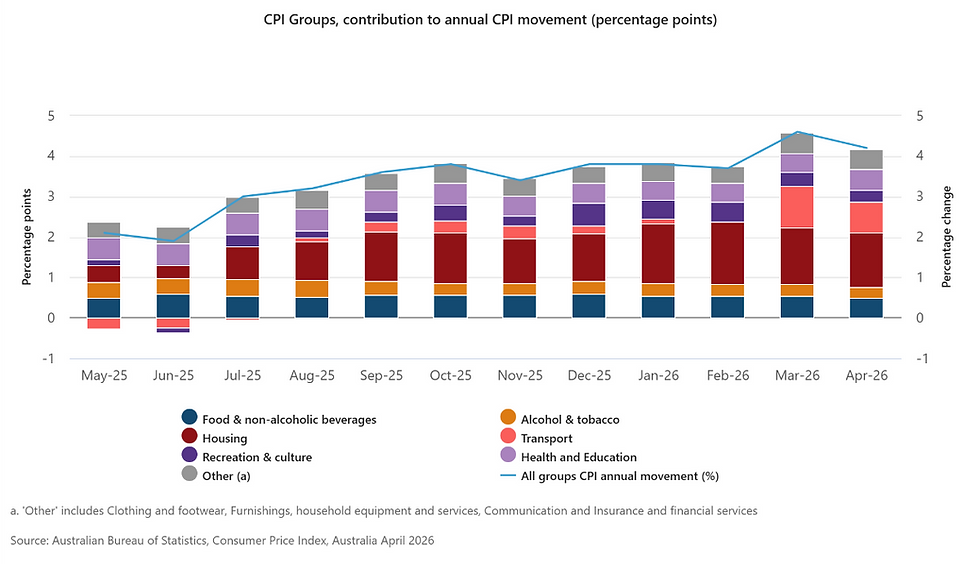

Housing, the highest-weighted group in the CPI, was the largest contributor to annual inflation in April at +6.3% yoy, reflecting rising costs for Electricity, New dwellings, and Rents.

Electricity costs are +22.5% higher than a year ago, as Commonwealth and State government rebates that reduced electricity costs for households are no longer in place.

This was followed by a +6.6% yoy rise in Transport, easing from an +8.9% rise in March.

Sue-Ellen Luke, ABS head of prices statistics, said: "Automotive fuel prices fell -7.0% from March to April, after rising by +32.8% yoy in the previous month. This month's fall includes the halving of the fuel excise on 1st April. Automotive fuel prices are still +23.5% higher compared to February and before the impact of the Middle East conflict. The impact of higher oil prices has also been seen in products and services with high freight and logistics costs, such as parcel delivery and building materials. This is reflected in price increases of +12.4% for Postal services and +4.7% for New dwelling construction compared to 12 months ago."

Food and non-alcoholic beverages rose by +2.8% yoy.

Goods inflation was down from +5.5% yoy in March to +4.7% in April. Services inflation was +3.5% yoy, slowing slightly from +3.6% yoy.

S&P/ASX200 8,669 +0.1%, AUDUSD 0.7165 (unch), Aus 2yr 4.52% -7bps, Aus 10yr 4.85% -6bps

Fin-X Wealth View

Australian CPI inflation was not as bad as feared for the second month in a row.

The government's decision to lower fuel excise has clearly helped reduce energy costs, easing some of the pressure after the initial increases. However, these are currently slated to end in June.

So far, the higher energy costs have had a muted impact on other sectors, notably services. We would expect inflation to continue to be passed through with a lag in the coming months. This implies that, despite the pleasing headline, inflation risks are still skewed to the upside later this year. In addition, the longer it takes to unblock the Strait of Hormuz, the more intense the risks become.

For the rest of the developed world, the issues primarily concern energy costs. However, in Australia, questions remain about the security of the energy supply. Last week's flash S&P Global PMI report revealed how worried businesses are about the flow and costs for the rest of the year. This has implications for both growth and inflation. Without energy supply, activities get cancelled, projects get delayed, and revenues could suffer.

Despite the higher inflation risks, the more positive takeaway is that slightly lower inflation and slightly higher unemployment are likely to keep the RBA on hold for now. If inflation picks up later this year, we still expect them to respond. But there's no urgent need to act. If a peace agreement were reached tomorrow, the RBA might be able to abandon plans for further rate hikes altogether.

Disclaimer

The contents of this communication is prepared by Brerona Capital Asset Management Pty Ltd (A.C.N. 627 650 293; AFSL 520526). The information contained in this communication is general in nature and does not take into consideration any investors personal objectives, goals, needs and financial situation. You should not rely on the information contained in this document to make any investment decisions without first consulting an investment professional such as your financial adviser. Any unauthorised use of this document is prohibited. This document (including any attachments) is intended only for the addressee, it may contain information of a privileged and confidential nature. If you are not the addressee of this communication, you must not copy, reproduce, disseminate or use this email and its contents. If this communication has been received in error by you, please inform us immediately and securely delete. Sharing, transmitting, copying, disseminating all or part of the contents of this document may result in a breach of the Federal Privacy Legislation and or copyright and trademark infringement of Brerona Capital Asset Management Pty Ltd and its related entities.