Fin-X Weekly 30th March 2026

- Brett Careedy

- Mar 30

- 5 min read

The Middle East conflict remained the dominant driver of markets, lifting energy prices and pressuring equities and bonds. Diplomatic efforts continued, but the gap between US and Iranian positions remains wide. Markets also absorbed signs of a broader regional escalation.

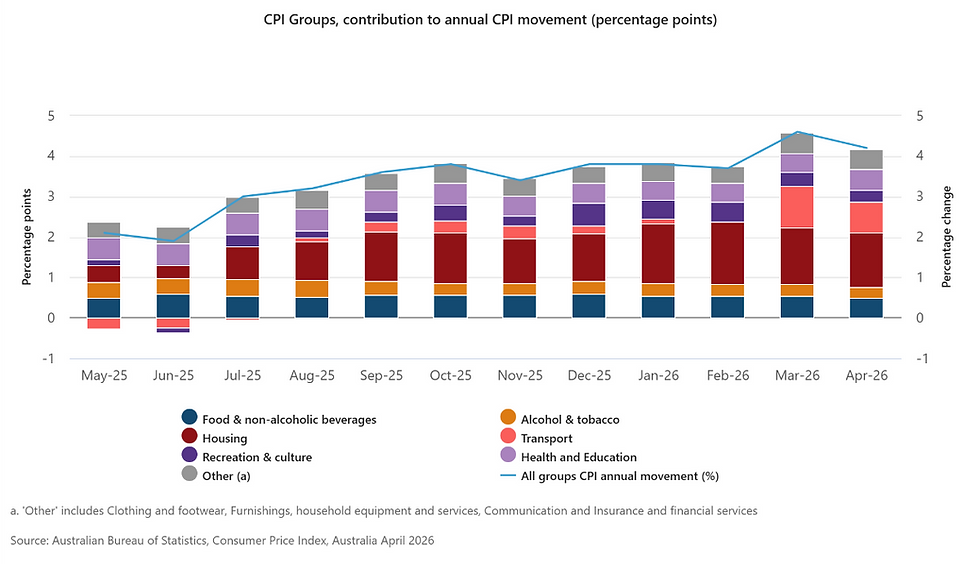

Australian inflation was weaker than anticipated in February but is expected to surge once energy prices are reflected.

Flash PMI data pointed to weaker growth and rising input costs across major economies. Rate markets responded by pricing a greater chance of further monetary tightening.

This week’s focus is likely to remain on the Persian Gulf. However, there will also be updated US retail sales and labour data, the ISM manufacturing survey, RBA minutes, Chinese PMIs, and Japanese activity figures.

Investor sentiment was subdued at Monday’s open after President Trump gave Iran an ultimatum to fully reopen the Strait of Hormuz by Tuesday or he would instruct US forces to “hit and obliterate” its power plants, starting with the largest facilities. Iran responded that it would lay mines across the “entire Persian Gulf” if further attacks hit its coastline.

Energy prices continued to rise, and miners suffered heavy losses as diesel input costs increased. Bond yields rose, while the South Korean KOSPI index fell by as much as -6.5% in local currency terms.

Risk appetite improved sharply after the president suspended his demands for five days to allow peace talks to take place. That recovery faded quickly as it became clear there was still distance between the negotiating positions.

The US reportedly communicated a 15-point peace plan through Pakistan, while Iran rejected the conditions and responded with its own list of demands. These included payment of war reparations and recognition of Iran’s sovereignty and control over the Strait of Hormuz. Tehran continues to frame control of this chokepoint as a key guarantee for enforcing any eventual agreement.

It also emerged that more American forces were being committed to the region, with signs that Saudi Arabia and the UAE were also preparing to enter the conflict.

On Friday, the price of Brent crude climbed above $110.0 per barrel once again after hopes of a swift resolution were dashed.

Meeting his G7 counterparts in France, Secretary of State Marco Rubio said that the war could take “weeks, not months”, and the president failed to calm markets by delaying infrastructure strikes for another ten days to allow more time for talks.

Pakistan has said it would host a meeting of Middle Eastern powers on Monday in an effort to find a regional approach to ending the conflict. The talks bring together the foreign ministers of Saudi Arabia, Turkey and Egypt. Still, they did not appear to include any of the warring parties, adding to doubts around persistent US claims of diplomatic progress.

After sharp falls in Friday’s Wall Street session, futures pricing was already indicating that the Australian share market would open in the red later today. However, news over the weekend that Iran-backed Yemeni Houthis had entered the conflict by firing missiles into Israel is likely to weigh further on risk sentiment this week. The widening of the conflict raises the prospect that shipping through the Suez Canal may also be interrupted.

Events in the Gulf overshadowed the conclusion of a trade agreement between Australia and the European Union. The deal drew criticism for not permitting enough Australian meat products to be exported, despite the EU remaining notably protective of its agricultural markets.

Global markets are now bracing for the effects of the war to appear in inflation data. There was at least some relief for Australians in the monthly CPI figures for February, which suggested inflation would not have reached the RBA’s mid-year estimate of +4.2% yoy were it not for the energy shock. However, the Treasurer conceded that inflation is likely to surge above +5.0% yoy as the impact of higher energy prices flows through.

The Prime Minister announced new fuel security powers to get “fuel restocked”, so Australia is “ready for what may come”. Mr Albanese said the new powers will allow the government to “underwrite the purchase of fuel by the private sector”. He also called a second emergency National Cabinet meeting to discuss the coordinated response between Canberra and the states.

The Treasurer confirmed that tax changes will be announced in the May 2026 budget but said no decision has yet been made on whether a reduction in the capital gains tax discount will be among them.

The first signs of a synchronised shock emerged in the flash S&P Global PMI surveys, which showed how the fallout from the Iran war is damaging growth momentum while also lifting input prices.

Multiple March reports showed declines, and composite measures for the US and the euro zone came in below economists’ expectations. The US report suggested GDP growth may be constrained to near 1.0% annualised during the first quarter.

Australia’s services gauge slumped to 46.6, signalling a sudden contraction, while Indian factory activity slowed to its weakest level since 2021.

As the conflict in the Middle East appears likely to drag on for some time, interest rate markets are increasingly pricing in global monetary policy tightening. Six of the G10 central banks are now assigned an above-even chance of raising rates at their next meeting, including the RBA, ECB, Bank of Japan and Bank of England, though not the Federal Reserve.

In other notable news, US private credit outflows and losses continued to weigh on sentiment. Deutsche Bank’s Ozan Tarman said on the Bloomberg Odd Lots podcast that if it were not for the conflict with Iran, strains in private credit would be the primary focus of macro investors, not an obscure side story.

In Los Angeles, a jury also found that Meta and Alphabet bore some legal responsibility for a 20-year-old woman's mental health struggles, which she said were caused by her addiction to social media. The verdict shows the potential multibillion-dollar exposure from lawsuits claiming that social media platforms are intentionally designed to addict young users without regard for their well-being.

The week ahead brings a comparatively heavier data flow despite the Easter-shortened calendar. Releases include the US labour market and JOLTS reports, the ISM survey and Retail Sales figures. In Australia, the latest RBA minutes will be published alongside trade data. China will release the official and RatingDog PMI surveys, and Japan will publish its key monthly activity data before the Tankan survey arrives with the start of the second quarter on Wednesday.

Disclaimer

The contents of this communication is prepared by Brerona Capital Asset Management Pty Ltd (A.C.N. 627 650 293; AFSL 520526). The information contained in this communication is general in nature and does not take into consideration any investors personal objectives, goals, needs and financial situation. You should not rely on the information contained in this document to make any investment decisions without first consulting an investment professional such as your financial adviser. Any unauthorised use of this document is prohibited. This document (including any attachments) is intended only for the addressee, it may contain information of a privileged and confidential nature. If you are not the addressee of this communication, you must not copy, reproduce, disseminate or use this email and its contents. If this communication has been received in error by you, please inform us immediately and securely delete. Sharing, transmitting, copying, disseminating all or part of the contents of this document may result in a breach of the Federal Privacy Legislation and or copyright and trademark infringement of Brerona Capital Asset Management Pty Ltd and its related entities.