Fin-X Rapid Response 26th March 2026

- Brett Careedy

- Mar 26

- 3 min read

Australian CPI was slightly below estimates in February, but excludes the impact of the energy price shock. CPI is set to rise, but the shock may yet prove to be deflationary over the medium term based on recent surveys.

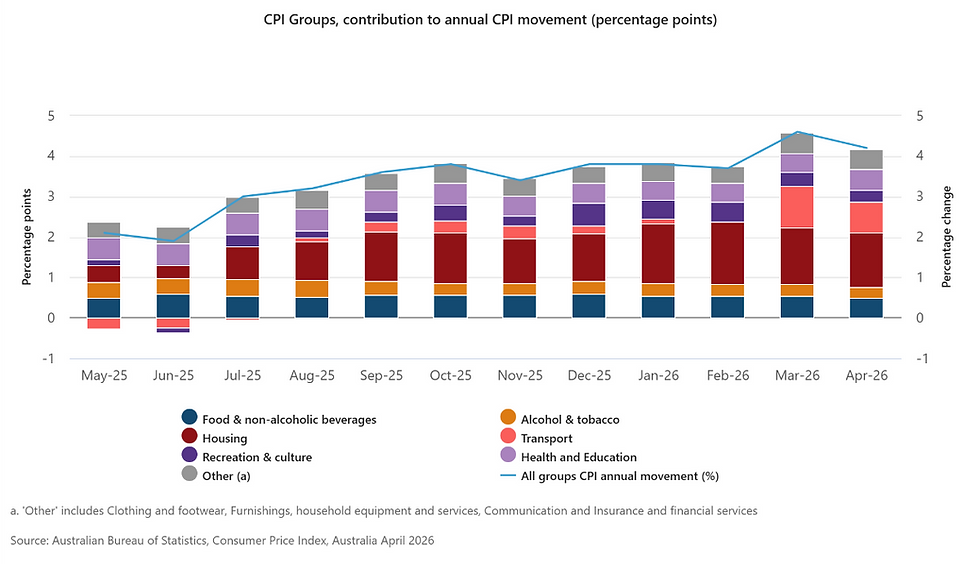

Today's monthly Australian CPI estimate cooled from +3.8% yoy in January to +3.7% yoy in February, according to the ABS. Economists polled by Bloomberg had expected it to remain at +3.8% yoy.

Trimmed mean CPI inflation also came in -0.1% below expectations, holding at January's downwardly revised +3.3% yoy.

The largest contributors to annual inflation were Housing (+7.2%), Food and non-alcoholic beverages (+3.1%) and Recreation and culture (+4.1%).

The increase in Housing was up from a +6.8% rise in the 12 months to January 2026. The main contributors to the annual rise were Electricity (+37.0%), New dwellings (+3.7%) and Rents (+3.8%).

The annual rise in electricity costs is primarily related to Commonwealth and State Government electricity rebates being used up by households. This is up from a +32.2% rise in the 12 months to January 2026.

Excluding the impact of the Commonwealth and State Government electricity rebates over the previous year, electricity prices rose +4.9% in the 12 months to February. This reflects annual price reviews by energy retailers in July 2025.

In monthly terms, electricity costs rose 1.0% in February 2026. The rise this month was driven by Perth electricity (+11.0%), as some households received the extended EBRF rebates in January 2026 in lieu of not receiving a payment in October 2025.

Today, the Treasurer said that inflation is likely to rise above +5.0% yoy as a consequence of the spike in energy prices.

S&P/ASX200 8,534 +1.9%, AUDUSD 0.6971 -0.4%, Aus 2yr 4.63% -10bps, Aus 10yr 4.95% -9bps

Fin-X Wealth View

Today's report could provide some relief to the RBA since, taken at face value, it suggests that CPI inflation was not marching steadily higher towards the mid-year peak of +4.2% yoy forecasted in February. It appeared to be peaking at a lower level before the energy price increase in March.

One small caveat is that the RBA doesn't take the monthly series as seriously as the quarterly series. A bigger caveat is that the February forecasts will be revised much higher as a consequence of the rise in energy costs.

Yesterday, S&P Global published its latest flash PMI report, which saw the services series drop from an expansionary reading of 52.8 in February to a sharply contractionary 46.6 in March. The rise in input costs was attributed as the main reason for the drop, alongside a drop in demand for Australian goods and services.

The report was the latest in a series of consumer and business surveys indicating that the combined impact of the February and March rate increases and the rise in energy costs is more likely to be contractionary and disinflationary, rather than being absorbed by demand and potentially inflationary.

At the March meeting, the RBA hadn't modelled the impact of an energy price shock. At the next meeting in early May, it seems likely that the forecasts will include an expected rise in CPI inflation and a significant rise in unemployment.

The market is pricing a 70% chance of another rate rise in May and a total +0.55% of rate rises by the end of the year. We judge that the risk is skewed more to the downside than the upside, unless the Treasurer provides more fiscal affordability relief in the upcoming Budget.

Disclaimer

The contents of this communication is prepared by Brerona Capital Asset Management Pty Ltd (A.C.N. 627 650 293; AFSL 520526). The information contained in this communication is general in nature and does not take into consideration any investors personal objectives, goals, needs and financial situation. You should not rely on the information contained in this document to make any investment decisions without first consulting an investment professional such as your financial adviser. Any unauthorised use of this document is prohibited. This document (including any attachments) is intended only for the addressee, it may contain information of a privileged and confidential nature. If you are not the addressee of this communication, you must not copy, reproduce, disseminate or use this email and its contents. If this communication has been received in error by you, please inform us immediately and securely delete. Sharing, transmitting, copying, disseminating all or part of the contents of this document may result in a breach of the Federal Privacy Legislation and or copyright and trademark infringement of Brerona Capital Asset Management Pty Ltd and its related entities.