Rapid Response - RBA cuts as expected, downgrades GDP forecasts

- Brett Careedy

- Aug 13, 2025

- 4 min read

As widely expected today, the RBA cut the overnight cash rate by a quarter point to 3.6%. Compared to May, the updated SMP focused less on trade and more on poor productivity growth, as GDP forecasts were downgraded over the horizon through to 2027.

At its meeting today, the Board unanimously decided to lower the cash rate target by -0.25% to 3.60%. The cash rate is now down -0.75% in 2025. A larger cut was not discussed.

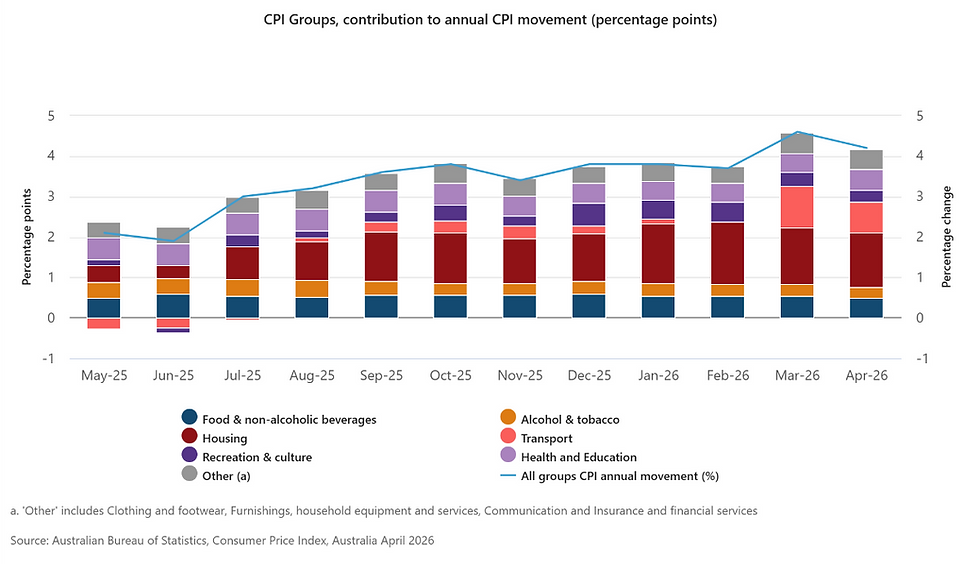

The Governor's statement highlighted that consumer price inflation had continued to moderate since the 2022 peak. Headline CPI is forecast (in the updated quarterly forecasts) to rise to 3.1% as electricity subsidies expire. Core trimmed mean inflation is expected to gravitate to and stabilise at the midpoint of the 2%-3% target range. The forecasts were based on market pricing of a gradual easing in the cash rate.

The Governor continued: "Uncertainty in the world economy remains elevated. There is a little more clarity on the scope and scale of US tariffs and policy responses in other countries, suggesting that more extreme outcomes are likely to be avoided. Trade policy developments are nevertheless still expected to have an adverse effect on global economic activity, and there remains a risk that households and firms delay expenditure pending still greater clarity on the outlook. As in May, the forecasts assume that both effects weigh on activity and inflation in Australia for a period."

Other observations summarised in the statement included a gradual easing in financial conditions, some tightness but easing in the labour market, pockets of weakness in some unspecified sectors, risks of slowing consumption, and uncertainties related to the lags with which monetary policy translates to higher activity.

On the policy outlook, the Governor concluded: "With underlying inflation continuing to decline back towards the midpoint of the 2–3 per cent range and labour market conditions easing slightly, as expected, the Board judged that a further easing of monetary policy was appropriate. This takes the decline in the cash rate since the beginning of the year to 75 basis points. The Board nevertheless remains cautious about the outlook, particularly given the heightened level of uncertainty about both aggregate demand and potential supply. It noted that monetary policy is well placed to respond decisively to international developments if they were to have material implications for activity and inflation in Australia."

In the Statement on Monetary Policy, the CPI outlook was essentially unchanged since May. However, the GDP growth forecasts were revised lower, with 2025 growth expected at +1.7% instead of +2.1%.

Slower growth in major trading partners in late 2025 (+2.8%) is expected to be slightly higher by the end of 2026 (+3.4%).

On domestic growth, the SMP said "The forecast pick-up in GDP growth over 2025 is now more gradual than expected in May, as weaker-than-expected growth in public demand in early 2025 is not expected to be offset through the rest of the year. We have also lowered our assumption for the medium-term (end of forecast period) rate of productivity growth as we assess that the persistent headwinds that have lowered productivity growth over recent decades are likely to continue over the next couple of years. This downgrade directly flows into our estimate of potential output growth and our forecast for GDP growth in 2026/2027 [...] "Year-ended GDP growth is expected to continue to pick up over the next year to around its potential growth rate; private demand growth is forecast to be a bit stronger than it has been over the past year, with public demand continuing to support growth [...] We judge that the economy will be close to full employment over the forecast period, though our models and some indicators point to the risk that some tightness in labour market conditions remains."

Earlier today, the NAB business survey showed that confidence rose to the highest level since August 2022.

US CPI is due out tonight, with the consensus view that headline CPI will tick up from +2.7% yoy to +2.8% yoy, with core CPI also expected to increase by +0.1% to +3.0% yoy.

Fin-X Wealth View

Compared to the recent period of higher inflation, the central message is that the economy is coming back into better balance.

The inflation forecasts and economic growth seem strangely steady, given the high uncertainty. The Governor commented on the potential for shocks, notably from US trade policy. Tariffs were cited as number 1 in the key risks to the SMP outlook.

Higher domestic excess demand was also cited as a risk, suggesting that the RBA is still more worried about inflation than growth and employment.

At the press conference, she also said that equity markets were surprisingly sanguine, given the risks that were presented. It is hard to disagree with this point, although elevated liquidity seems to be the most likely cause.

Bond yields held steady. Market pricing still suggests that the cash rate will bottom at 3% in mid-2026.

Source: Bloomberg, NAB, 12th August 2025

Disclaimer

The contents of this communication is prepared by Brerona Capital Asset Management Pty Ltd (A.C.N. 627 650 293; AFSL 520526). The information contained in this communication is general in nature and does not take into consideration any investors personal objectives, goals, needs and financial situation. You should not rely on the information contained in this document to make any investment decisions without first consulting an investment professional such as your financial adviser. Any unauthorised use of this document is prohibited. This document (including any attachments) is intended only for the addressee, it may contain information of a privileged and confidential nature. If you are not the addressee of this communication, you must not copy, reproduce, disseminate or use this email and its contents. If this communication has been received in error by you, please inform us immediately and securely delete. Sharing, transmitting, copying, disseminating all or part of the contents of this document may result in a breach of the Federal Privacy Legislation and or copyright and trademark infringement of Brerona Capital Asset Management Pty Ltd and its related entities.