Fin-X Weekly Update 9th February 2026

- Brett Careedy

- Feb 9

- 5 min read

Market volatility increased due to several factors that weighed on investor sentiment last week, although risk appetite returned in Friday’s session.

The RBA became the first major central bank to raise interest rates since the post-COVID inflation spike, but the governor emphasised it would be cautious going forward.

The US labour report was delayed until this week due to the short government shutdown. However, last week’s data suggested that the American labour market is softening.

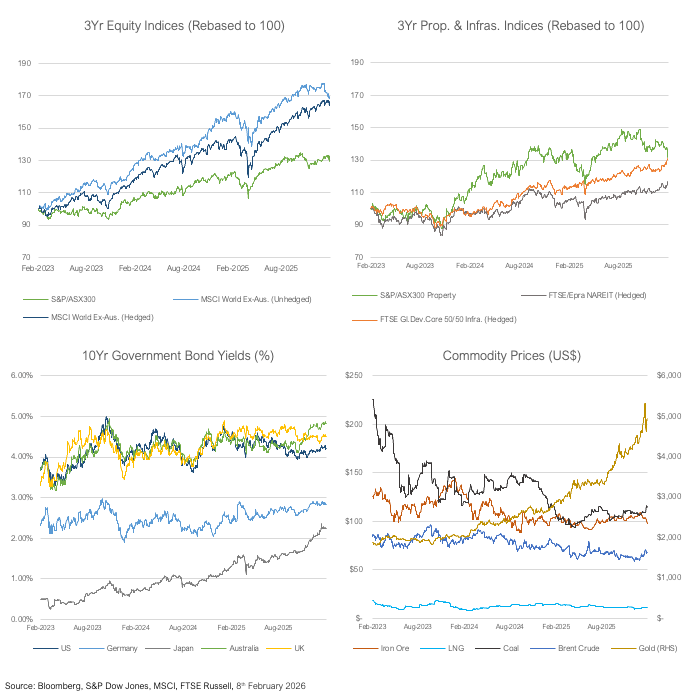

Consumer spending figures in the US and Australia will be closely watched this week, along with US & Chinese inflation data, and European production figures. The NAB business and Westpac consumer surveys will be published tomorrow.

Global risk appetite soured last week amid a combination of concerning US macroeconomic data and revelations about new AI tools.

For Australians, the news was dominated by the RBA’s first rate increase since November 2023, which raised the cash rate from 3.60% to 3.85% and supported the Aussie dollar. As the ECB and Bank of England kept rates on hold and retained a neutral and dovish tilt, respectively, Australia’s Reserve Bank became the first major central bank to raise rates since the post-COVID inflation spike.

The governor opened the press conference by saying, “The recent run of data gives the board a clear enough view that the underlying pulse of inflation is too strong. We’ve updated our assessment and outlook for the economy and concluded that the cash rate was no longer at the right level to get inflation back to target in a reasonable time frame." However, the tone was a little less hawkish as she took questions, emphasising that the Board would be cautious in its approach.

The updated quarterly forecasts were, as usual, based on the market-implied interest rate path, which plotted the cash rate rising to 4.25% in mid-2027. Under this assumption, CPI inflation is expected to peak around 4.2% in the middle of this year, before gradually returning to the 2%-3% target range over the next 12 months. However, GDP growth is expected to slow from +2.3% to +1.6%, with unemployment rising to 4.6% in 2028. Investors appeared to understand that the Reserve Bank would be comfortable with this outcome, as interest rate expectations changed little following the meeting.

The RBA's central concern is that the economy's productive capacity has not kept pace with demand, leading to upward price pressures. As public-sector demand faded in 2025, private-sector demand has accelerated more than previously envisaged. The governor attributed this to a faster response to last year's interest rate rises, although population growth is also likely to have contributed.

A rise in January job advertisements appeared to support the central bank’s outlook and provided a contrast to the decline in US December job openings.

Early in the week, there was an apparently upbeat headline ISM manufacturing survey, supported by a boost in new orders. However, the ISM services figures and supporting anecdotal excerpts were far less optimistic, coinciding with a spike in Challenger job cuts to +108k, more than double the level of a year ago.

Delayed by a short partial government shutdown, this week's labour report is expected to show that unemployment remained at 4.4% in January. However, a much weaker-than-anticipated ADP private payrolls survey (+22k) indicates some upside risk to the unemployment figures.

In another blow for the employment outlook, Goldman Sachs reported that engineers from Claude developer Anthropic had been working on autonomous systems for time-intensive, high-volume back-office work. The bank expects efficiency gains rather than near-term job cuts, using AI to speed up processes and limit future headcount growth. The success of the AI agents apparently surprised executives, reinforcing the idea that AI can handle complex, rules-based work such as accounting and compliance.

Released on Friday, the Goldman Sachs story helped the market rebound from an earlier sell-off stemming from the possible negative impacts on the software sector. Anthropic’s legal automation tool threatens to supplant established data and SaaS players, such as Thomson Reuters, which fell by -20.4% over the week in US dollar terms.

Even after the rebound, big tech players still saw their share prices finish the week lower despite generally positive results.

Alphabet’s (-4.5%) Q4 earnings and revenue beat Wall Street expectations, with its cloud unit generating a +48% increase in revenue.

Palantir jumped by more than +10% after the defence company gave strong fourth-quarter financial results and upbeat guidance, but still reversed to end the week -7.3% lower.

Similarly, AMD (-12.0%) beat forecasts but issued guidance that fell short of lofty expectations, even as CEO Lisa Su said, “AI is accelerating at a pace that I would not have imagined.”

Amazon (-12.1%) slightly missed analyst expectations and said that it would invest approximately US$200 billion this year. Walmart (+10.1%) nevertheless topped a US$1 trillion valuation after reporting that it was successfully growing its online channels and sales to higher-income customers, with capital investments at a more modest US$23-26 billion. The company also likely benefited from the transfer of its listing from the NYSE to the Nasdaq in December.

High capital expenditures are troubling investors, who can see issues emerging in the debt-financing sector. For example, BlackRock’s business development company, BlackRock TCP Capital Corp., disclosed an estimated -19% reduction in its net asset value for Q4, driven by significant write‑downs on several troubled loans. At the same time, major tech lender Blue Owl has seen its share price slip by -16.2% so far this year, after falling by -35.8% in 2025.

The credit concerns are adding to liquidity issues that have seen the value of liquidity-sensitive assets retrace from recent peaks. Gold ended the week back below US$5,000 per oz, while the price of bitcoin has fallen by more than -45% from its October peak.

Despite a backdrop that appears more hostile to high valuations, Elon Musk’s SpaceX is reported to have acquired his artificial intelligence startup xAI, which also owns the X platform formerly known as Twitter, valuing the company at US$1.25 trillion and consolidating his private holdings outside of Tesla. The transaction comes ahead of an initial public offering for SpaceX later this year. Musk said a main reason for the merger was to better build “orbital data centres”.

In other M&A news, Rio Tinto has abandoned talks to acquire Glencore after the two sides failed to agree on valuation, scuttling a merger that would have created the world’s largest mining company. Rio Tinto added +3.7% while Glencore dropped by -5.5% over the week in Australian dollar terms.

With 291 S&P 500 companies now having reported, aggregate earnings are up +13.6% compared to a year ago. McDonald's and Airbnb are among the 79 companies scheduled to publish results this week.

Besides the labour report, which will include the annual benchmark revisions, US retail sales and CPI figures will also be released this week, along with Chinese inflation and European production data. Household spending figures are due later today in Australia, followed by the NAB business and Westpac consumer surveys tomorrow.

Significant Upcoming Data:

Disclaimer

The contents of this communication is prepared by Brerona Capital Asset Management Pty Ltd (A.C.N. 627 650 293; AFSL 520526). The information contained in this communication is general in nature and does not take into consideration any investors personal objectives, goals, needs and financial situation. You should not rely on the information contained in this document to make any investment decisions without first consulting an investment professional such as your financial adviser. Any unauthorised use of this document is prohibited. This document (including any attachments) is intended only for the addressee, it may contain information of a privileged and confidential nature. If you are not the addressee of this communication, you must not copy, reproduce, disseminate or use this email and its contents. If this communication has been received in error by you, please inform us immediately and securely delete. Sharing, transmitting, copying, disseminating all or part of the contents of this document may result in a breach of the Federal Privacy Legislation and or copyright and trademark infringement of Brerona Capital Asset Management Pty Ltd and its related entities.