Fin-X Weekly 13th April 2026

- Brett Careedy

- Apr 13

- 5 min read

A two-week pause in Middle East hostilities lifted risk appetite, drove oil prices lower and stocks higher last week. That relief remains tentative as negotiations between the US and Iran have broken down and tensions around the Strait of Hormuz persist.

US inflation picked up sharply as higher energy prices fed into March CPI, while Q4 GDP was revised down and consumer sentiment hit an all-time low. Australian household spending slightly undershot expectations ahead of the full impact of higher energy costs, while markets continue to price in further RBA tightening.

Stock headlines included Meta’s new AI model launch and Anthropic’s decision to restrict the release of Claude Mythos on safety grounds.

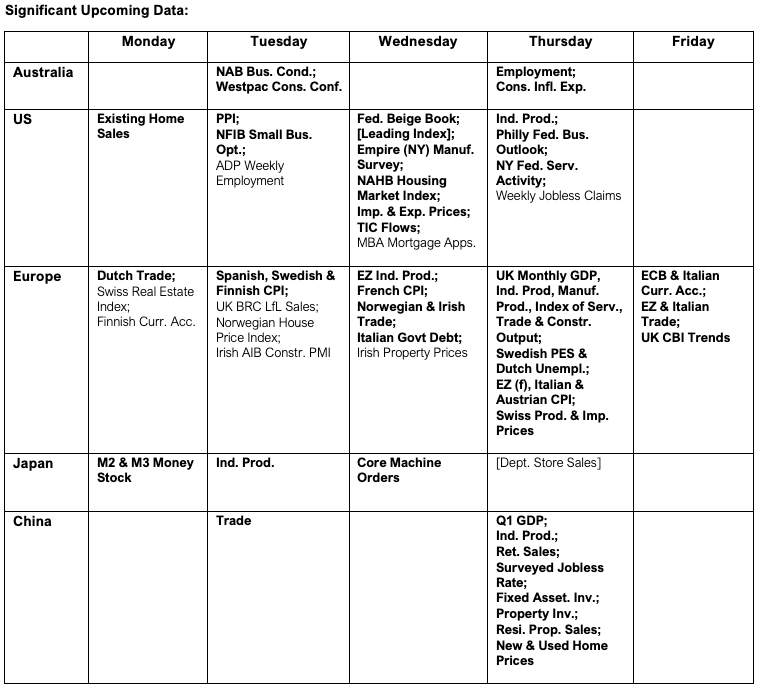

This week’s focus will remain primarily on the Middle East, along with US bank earnings, the IMF Spring Meetings, central bank speeches, Australian employment data, US PPI and industrial production, and Chinese Q1 GDP figures.

Risk appetite rebounded after the US and Iran announced a two-week pause in hostilities in the Persian Gulf on Wednesday. Oil prices tumbled, equities surged, and the US dollar erased most of its 2026 gains. Sentiment also strengthened early in the week after the minutes of the mid-March Federal Reserve meeting indicated that FOMC members remained inclined to cut US dollar interest rates later this year. Emerging markets were the main beneficiary, rising by +7.6% over the week in Australian dollar terms.

The improvement in sentiment sat alongside clear signs that the ceasefire was fragile from the outset. Iran accused Israel of breaching the terms as attacks on Hezbollah continued in southern Lebanon. Strikes then hit Saudi energy infrastructure, while the Iranian military crucially retained control of the Strait of Hormuz.

The US also faced international criticism for appearing open to giving Iran control of the Strait, something Iran did not possess at the end of February before American strikes began.

Vice President J.D. Vance travelled to Pakistan over the weekend to meet Iranian negotiators. He later announced that no agreement had been reached after 21 hours of talks. Iran also criticised the Americans for maintaining maximalist demands, prompting speculation that the pause in hostilities may be serving only to buy time for additional troops to arrive in the region. The parties will now return home after the breakdown in negotiations, and risk sentiment could weaken at the open later today.

Last week also brought the first US inflation figures to reflect the impact of higher energy prices. According to the BLS, US March CPI rose to +3.3% yoy from +2.4% yoy a month earlier, although the result came in slightly below consensus estimates. Even so, it marked the largest monthly increase since 2022, with gasoline prices surging +21.2% in March.

That inflation outcome came against a softer backdrop for activity. The BEA’s estimate of Q4 GDP was revised down from +0.7% to +0.5% at an annualised pace, adding to concerns about the underlying strength of the US economy.

Conditions for the US consumer remain strained. Real disposable personal income fell by -0.5% in February, the personal saving rate declined to 4.0%, and real consumption rose by only +0.1%. Taken together, those readings suggest households have limited capacity to absorb further price shocks without demand slowing. The University of Michigan consumer sentiment survey also fell to the lowest level on record as affordability concerns intensified.

Australian household spending data also pointed to softer momentum. ABS figures showed household spending rose +4.6% yoy in nominal terms in February, slightly below expectations. The data preceded the rise in energy costs but coincided with the RBA’s first of two rate rises this year. Australian consumers are expected to face even greater pressure in the months ahead, with at least two further rate rises still priced in for this year.

In New Zealand, the RBNZ left the cash rate unchanged at 2.25% on Wednesday, in line with expectations, but adopted a more hawkish bias. The Bank said that "decisive and timely increases in the [cash rate] would be required" if core inflation, inflation expectations, or wage growth moved out of line with its 2% medium-term target.

AI news led company developments last week. Meta unveiled Muse Spark, its first major AI model under the revamped Meta Superintelligence Labs led by Scale AI co-founder Alexandr Wang. The release was an important step for Meta as it seeks to reinforce its position in the race to develop more capable frontier systems and show that the restructuring of its AI efforts is beginning to produce tangible results.

Even so, Meta’s announcement was overshadowed by developments at Anthropic. The company said it would not immediately release its Claude Mythos model after safety tests uncovered capabilities that it considered too concerning for broad deployment. Rather than proceeding with a general release, Anthropic will deploy Mythos through a new initiative called Project Glasswing.

Access under Project Glasswing will be limited to roughly 50 organisations, including Amazon, Apple, Microsoft, Broadcom, Cisco, CrowdStrike, the Linux Foundation and Palo Alto Networks. Those groups will use the model to scan their own critical software infrastructure for vulnerabilities before adversaries can weaponise comparable capabilities.

Treasury Secretary Scott Bessent and Federal Reserve Chair Jerome Powell convened a group of bank executives this week to ensure that major banks proactively strengthen their security posture before similar capabilities become more widely available.

The major US banks will begin the earnings season this week, providing an early read on credit conditions, consumer balance sheets, trading activity and management commentary on growth and provisioning.

With events in the Middle East still unresolved, markets are also likely to remain sensitive to any developments in energy supply, shipping routes, and the broader security backdrop.

Analysts will also be following the IMF Spring Meetings in Washington, D.C., the Hungarian election, and speeches from several central bankers.

On the data front, the main Australian business and consumer surveys are due tomorrow, followed by employment figures on Thursday. In the US, PPI and industrial production will be released. China will also publish Q1 GDP and activity numbers.

Disclaimer

The contents of this communication is prepared by Brerona Capital Asset Management Pty Ltd (A.C.N. 627 650 293; AFSL 520526). The information contained in this communication is general in nature and does not take into consideration any investors personal objectives, goals, needs and financial situation. You should not rely on the information contained in this document to make any investment decisions without first consulting an investment professional such as your financial adviser. Any unauthorised use of this document is prohibited. This document (including any attachments) is intended only for the addressee, it may contain information of a privileged and confidential nature. If you are not the addressee of this communication, you must not copy, reproduce, disseminate or use this email and its contents. If this communication has been received in error by you, please inform us immediately and securely delete. Sharing, transmitting, copying, disseminating all or part of the contents of this document may result in a breach of the Federal Privacy Legislation and or copyright and trademark infringement of Brerona Capital Asset Management Pty Ltd and its related entities.