Fin-X Pulse - RBA surprises with a hold, but more easing to come

- Brett Careedy

- Jul 9, 2025

- 5 min read

Updated: Jul 16, 2025

The market had priced an 88% probability of a rate cut today. However, the RBA surprised investors by holding rates at 3.85% after a split decision by the Board. Nevertheless, the Governor anticipates that monetary easing will continue at a gradual pace unless the Board is forced to respond to negative shocks with more aggressive cuts.

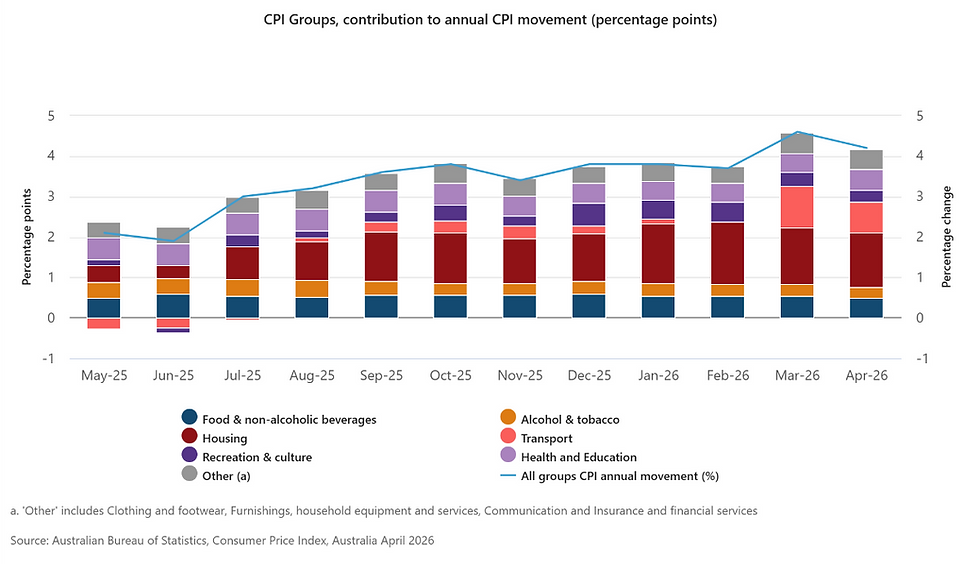

After acknowledging that inflation had continued to moderate, the Governor's statement said: "In the March quarter, headline inflation, which has partly been affected by temporary cost of living relief, was at the midpoint of the target range while trimmed mean inflation was at 2.9 per cent. The baseline forecast in May was for underlying inflation to continue to moderate to around the midpoint of the 2–3 per cent range with the cash rate assumed to follow a gradual easing path. While recent monthly CPI Indicator data suggest that June quarter inflation is likely to be broadly in line with the forecast, they were, at the margin, slightly stronger than expected. With the cash rate 50 basis points lower than five months ago and wider economic conditions evolving broadly as expected, the Board judged that it could wait for a little more information to confirm that inflation remains on track to reach 2.5 per cent on a sustainable basis." [Emphasis added]

Highlighting US policy uncertainties: "Uncertainty in the world economy remains elevated. While the final scope of US tariffs and policy responses in other countries remains unknown, financial market prices have rebounded with an expectation that the most extreme outcomes are likely to be avoided. Trade policy developments are nevertheless still expected to have an adverse effect on global economic activity, and there remains a risk that households and firms delay expenditure pending greater clarity on the outlook."

Despite some weakness in domestic demand: "Uncertainty in the world economy remains elevated. While the final scope of US tariffs and policy responses in other countries remains unknown, financial market prices have rebounded with an expectation that the most extreme outcomes are likely to be avoided. Trade policy developments are nevertheless still expected to have an adverse effect on global economic activity, and there remains a risk that households and firms delay expenditure pending greater clarity on the outlook." [Emphasis added]

On the labour market: "Various indicators suggest that labour market conditions remain tight. [...] Wages growth has softened from its peak but productivity growth has not picked up and growth in unit labour costs remains high."

The statement highlighted uncertainty in the evolution of domestic economic activity and the impacts of the monetary easing that had already occurred.

Explaining the decision to hold: "The Board continues to judge that the risks to inflation have become more balanced and the labour market remains strong. Nevertheless it remains cautious about the outlook, particularly given the heightened level of uncertainty about both aggregate demand and supply. The Board judged that it could wait for a little more information to confirm that inflation remains on track to reach 2.5 per cent on a sustainable basis. It noted that monetary policy is well placed to respond decisively to international developments if they were to have material implications for activity and inflation in Australia." [Emphasis added]

At the press conference, the Governor added that today's decision was "about timing more than direction". The base case remains a "cautious and gradual approach to easing monetary policy."

Earlier today, the NAB business conditions survey leapt from 0 to 9, the highest level since March last year, driven by improved trading, profitability, capacity utilisation. and employment. Business confidence also improved.

The decision also followed the announcement that the US would delay implementation of the latest higher levels of tariffs until 1st August.

S&P/ASX200 8,591 (unch), AUDUSD 0.6534 (unch), Aus 2yr 3.36% +11bps, Aus 10yr 4.26% +8bps

Fin-X Wealth View

Explaining today’s decision at the press conference, the Governor noted that recent monthly headline inflation estimates had dropped to +2.1% yoy, the low end of the RBA’s 2%-3% range. However, she emphasised that the Board was more focused on quarterly trimmed mean inflation which is seen as superior and remained at +2.9% at the end of March. She suggested that the RBA had interpreted recent data a little differently to the market, doubting the representative power of the monthly indicator due to factors including housebuilding costs, durable goods, and the impact of the electricity subsidies.

Quarterly core inflation rate had been within the target range for a relatively short period of time and the Board was unsure how the -0.5% of cuts already made since February would impact the path of future inflation. Notably, some of the components of the recent monthly series suggested that there might be some upside risk to the June figures. These figures will be released before the next meeting in August, when new quarterly forecasts will also be produced.

Activity has also held up better than anticipated. Significantly, the risks of a severe tariff-related downturn are judged to have abated. This assessment was supported by today's NAB survey.

But the 6-3 split in the votes only related to the timing of cuts, suggesting that an August cut is still likely. Interest rates are still on course to bottom around 3% in mid-2026.

However, the Governor also made repeated references to poor productivity performance, which may become a reason to lean a little more hawkish over the medium term if wage growth continues to rise.

Interestingly, the discussion revealed that it might be more difficult to guide the market on the path of future rates given the nature of the new Monetary Policy Board structure. Short-term surprises could well become more frequent.

Disclaimer

The contents of this communication is prepared by Brerona Capital Asset Management Pty Ltd (A.C.N. 627 650 293; AFSL 520526). The information contained in this communication is general in nature and does not take into consideration any investors personal objectives, goals, needs and financial situation. You should not rely on the information contained in this document to make any investment decisions without first consulting an investment professional such as your financial adviser. Any unauthorised use of this document is prohibited. This document (including any attachments) is intended only for the addressee, it may contain information of a privileged and confidential nature. If you are not the addressee of this communication, you must not copy, reproduce, disseminate or use this email and its contents. If this communication has been received in error by you, please inform us immediately and securely delete. Sharing, transmitting, copying, disseminating all or part of the contents of this document may result in a breach of the Federal Privacy Legislation and or copyright and trademark infringement of Brerona Capital Asset Management Pty Ltd and its related entities.