Fin-X Weekly 1st December 2025

- nav719

- Dec 1, 2025

- 5 min read

Risk assets rebounded as global markets moved to price in a December rate cut from the Federal Reserve.

American and Chinese data pointed to softer growth, despite signs of robust consumer spending over the holiday weekend.

Australian bond yields rose after stronger-than-expected inflation data led markets to rule out further RBA cuts, while APRA tightened mortgage lending standards.

In the week ahead, investors will focus on Australian GDP figures and a larger volume of delayed US data, including PCE inflation figures. There will also be a wide range of European inflation data, a likely rate cut in India, and possible peace talks between the US, Russia and Ukraine.

Global equities and other liquidity-sensitive assets found support in the days leading up to the American Thanksgiving weekend as markets began to reprice the likelihood of a Federal Reserve rate cut in December.

American indices were buoyed by a +6.8% rise in Alphabet’s share price after reports that an updated version of Google’s artificial intelligence model, Gemini 3, represents a significant leap ahead of its predecessor. The new system is said to post state-of-the-art scores across reasoning, maths, and multimodal benchmarks, outperforming OpenAI’s GPT-5.1 and Anthropic’s Claude 4.5 Sonnet. It also delivers substantial gains across a range of challenging benchmarks, pushing Google, for the first time, into the position of performance leader in the AI race.

At the same time, the company announced a deal to supply TPUs to Meta, underlining its ambition to deepen its presence across the broader AI ecosystem. Shares in chipmaker Nvidia slipped -1.1% over the week despite a +3.8% rally in the Nasdaq Composite index.

Global bond yields were mostly steady after a run of disappointing economic data and a Bloomberg report suggesting that National Economic Council Director Kevin Hassett is currently the leading candidate among five potential successors to Federal Reserve Chair Jerome Powell, whose term ends in May. The White House moved to downplay the speculation and emphasised that the decision remains open. Other shortlisted names include former Fed Governor Kevin Warsh, BlackRock executive Rick Rieder, and current Fed Governors Christopher Waller and Michelle Bowman.

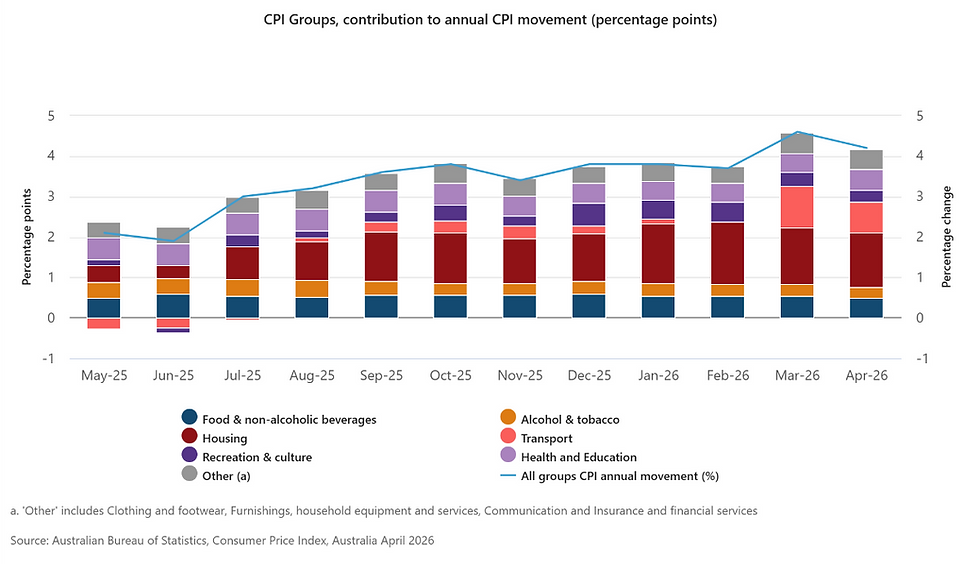

Australian bond yields rose after a substantial upside surprise in the first full monthly set of Australian CPI data produced by the ABS. Annual headline CPI rose by +3.8% to the end of October, up from +3.2% yoy at the end of September and ahead of market expectations of a +3.6% increase. Housing costs (+5.9%) were the most significant contributor, including a +37.1% rise in electricity prices due to distortions related to the timing of government subsidies. However, the increase was relatively broad-based, with the trimmed mean core CPI measure also rising by +3.3% yoy, above the consensus estimate and up from +3.0% in September.

Following the release, markets moved to exclude any further rate cuts from the RBA in this cycle. Friday’s RBA statistics subsequently showed that private credit growth accelerated to +7.3% in October, reinforcing the case for a more cautious stance. The Australian dollar appreciated in response to the likely more restrictive policy path. In parallel, APRA announced a home loan leverage cap, limiting mortgage loans of six or more times income to 20% of total lending, in an effort to cool the housing market and reduce financial stability risks.

In the United States, the dissemination of economic data is likely to gather pace after the long weekend. Last week, delayed September producer price data indicated muted inflationary pressures, with a +2.7% yoy increase as a pick-up in goods prices was offset by falling services costs. This week’s PCE inflation reading, the Fed’s preferred measure, is expected to show a +2.8% rise over the year to September and will be closely watched for confirmation that underlying price pressures continue to moderate.

Retail sales, which rose +4.3% yoy to September, were already showing signs of losing momentum. Early reports of Black Friday sales suggest that consumers are spending more than last year, with sizeable online discounts proving a significant draw. However, survey and labour data point to a more cautious backdrop. Earlier in the week, the Conference Board reported that consumers had become more pessimistic about current conditions and their prospects for the future, with growing concern about the ability to find a job. The weekly ADP report suggested that private companies lost an average of -13,500 jobs a week over the past four weeks.

The Federal Reserve’s Beige Book painted a similar picture. It reported that overall consumer spending had declined further, except among higher-end shoppers, while employment slipped slightly. Prices continued to rise moderately, but business outlooks were essentially unchanged. Together, these indicators point to a cooling US economy, with resilience concentrated in higher-income households.

In the United Kingdom, Chancellor Rachel Reeves’ budget provided an increased fiscal buffer. The budget effectively raised taxes on both ordinary workers and the wealthy to fund additional welfare spending and energy-bill support for lower-income households, with the most significant tax rises coming into effect just as Labour heads into the next general election. Investors reacted positively to the perceived prudence of the package, but there were few signs that it would materially brighten the country’s growth outlook. The plan offers little on structural reform and has attracted criticism for the absence of meaningful tax simplification.

Chinese data again underlined the challenges facing the world’s second-largest economy. Industrial profits fell -5.5% yoy in October, the biggest decline since June, after rising by +21.6% in September and +20.4% in August. Base effects somewhat exaggerated the scale of the reversal, but the direction underscored persistent pressure on corporate earnings.

In addition, the official non-manufacturing PMI slipped to just below 50, joining the manufacturing index in signalling a slight contraction across both parts of the economy. The weaker-than-expected readings highlight how China continues to grapple with lacklustre domestic demand and softer exports.

The coming week is likely to be busy for data and policy events. The tally of Black Friday and Cyber Monday sales will provide an early read on the strength of US holiday spending. ISM surveys and industrial production numbers are scheduled ahead of the PCE inflation release on Friday. At the same time, the calendar is also likely to be peppered with other data delayed by the earlier government shutdown.

In Australia, third-quarter GDP figures are due on Wednesday, with economists expecting annual growth to pick up from +1.8% in June to +2.2% in September.

Elsewhere, European inflation figures and Chinese RatingDog PMIs are expected, alongside a quarter-point rate cut from the Indian central bank.

Lastly, there is renewed hope that peace talks might be held between the US, Ukraine, and Russia

Disclaimer

The contents of this communication is prepared by Brerona Capital Asset Management Pty Ltd (A.C.N. 627 650 293; AFSL 520526). The information contained in this communication is general in nature and does not take into consideration any investors personal objectives, goals, needs and financial situation. You should not rely on the information contained in this document to make any investment decisions without first consulting an investment professional such as your financial adviser. Any unauthorised use of this document is prohibited. This document (including any attachments) is intended only for the addressee, it may contain information of a privileged and confidential nature. If you are not the addressee of this communication, you must not copy, reproduce, disseminate or use this email and its contents. If this communication has been received in error by you, please inform us immediately and securely delete. Sharing, transmitting, copying, disseminating all or part of the contents of this document may result in a breach of the Federal Privacy Legislation and or copyright and trademark infringement of Brerona Capital Asset Management Pty Ltd and its related entities.